Preventing Junk Beats Cleaning It: Life-Extension and End-of-Life Services Go Commercial

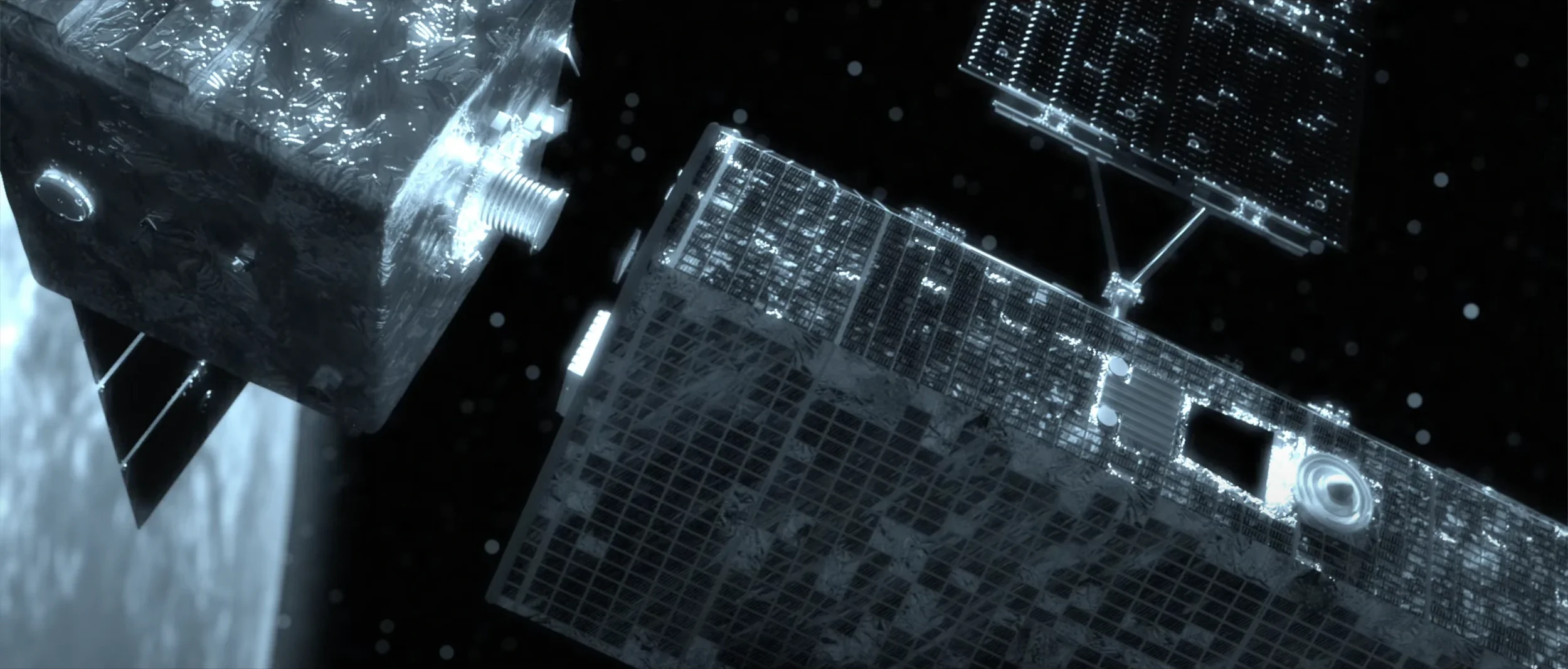

Astroscale proposes a magnetic docking system to catch decommissioned satellites and other debris in Earth orbit, and then release these in the atmosphere to burn up on re-entry.

Credit: Astroscale

From MEV in GEO to Astroscale’s ELSA-M in LEO, servicing is becoming a product line

If you want fewer derelicts in orbit tomorrow, servicing is the lever you can pull today. Two families of offerings are maturing fast: life-extension for high-value GEO assets and end-of-life (EOL) removal for LEO constellations prepared with capture interfaces. Together they reduce failures, delay uncontrolled deaths and make removals cheaper and safer when they do happen.

The proof point in GEO is Northrop Grumman’s Mission Extension Vehicle (MEV). MEV-1 docked with Intelsat IS-901 in 2020, providing several years of station-keeping and pointing; MEV-2 docked with IS-10-02 directly in the operational slot in 2021. In 2025, Intelsat and Northrop confirmed successful undocking and retirement of IS-901 after the extended service—exactly the life-cycle you want to see. This isn’t theory; it’s an audited, flown service with repeat customers.

In LEO, Astroscale’s ELSA-M is the bellwether. Backed by the UK Space Agency and ESA alongside commercial customers, ELSA-M completed Critical Design Review in June 2025 and is targeting a 2026 launch. The mission will demonstrate magnetic capture of prepared client satellites (Eutelsat OneWeb) equipped with docking plates—a practical standard that lets servicers rendezvous and remove multiple spacecraft in a single campaign. That combination—prepared clients plus a multi-removal servicer—turns sustainability into a repeatable SKU, not a bespoke caper.

Commercial implications follow quickly. For operators, life-extension protects revenue and defers capex; for insurers, it reduces risk of uncontrolled failures; for regulators, it creates credible pathways to meet de-orbit mandates. For constellation builders, adopting prepared-for-removal hardware (docking plates, grappling ridges, ferromagnetic paddles) shifts EOL from wish to plan. Airbus purchasing docking plates in bulk is a signal that primes see preparation as part of baseline design, not an optional extra.

Go-to-market that resonates is service-centred. Bundle on-orbit services as availability contracts: uptime guarantees in GEO with documented pointing margins; or LEO EOL packages with per-client pricing and defined removal windows. Publish rendezvous and proximity operations (RPO) interfaces and safety cases so operators can pre-qualify. And be explicit about partial-credit: even if weather or conjunctions delay a de-orbit, an operator can still value safe relocation to a lower perigee.

Policy is helping. The FCC’s 5-year rule tightens disposal timelines in LEO, and ESA’s Zero Debris Charter is converting sustainability pledges into procurement criteria across governments and industry. Vendors that align their service packs to these frameworks shorten sales cycles because compliance officers can read the mapping.

The category won’t replace ADR; it will feed it. Life-extension squeezes more value from GEO assets before controlled retirement; prepared EOL in LEO ensures removals are predictable and affordable. The net effect is fewer surprises, fewer derelicts, and a clearer cost curve for the clean-up missions we’ll still need.

The market signal is clear: when servicing is modular, insurable and documented, buyers show up. MEV proved it at GEO; ELSA-M aims to prove it in LEO. That’s how you prevent junk—by making “don’t create it” the easiest contract to sign.